The pandemic may lead some companies that have outsourced lots of operations to the cloud to go a step further and get rid of at least some offices. "I just don't think we are going to go back [to business as usual]", says Frank Slootman, boss of Snowflake, a database firm. Even digerati like Twitter plan to turn more virtual.

Still, some businesses suddenly forced into remote work will rue the experience, predicts Mr Gascoigne. Without a learning period they will get all the drawbacks and few of the benefits. Brainstorming and other creative activities are possible online but take practice—and even then feel like an imperfect ersatz of an actual room. Recruiting and breaking in new employees is hard virtually. According to one recent survey of 3,500 remote workers, one in five struggles with loneliness. That is partly why GitHub and Trello operate optional offices.

Most businesses will always have to be located somewhere and need people to work side by side. But as technology improves, swathes of the knowledge economy will gradually move more functions online,

Read the whole article, The nowhere firm, online here: https://www.economist.com/node/21782654?frsc=dg%7Ce

Bill Ackman's Pershing Square Capital Management hedge fund laid out $27 million to buy credit protection on global investment-grade and high-yield credit indexes. The purchases, which were made late last month when credit spreads were tighter, carried limited downside risk but the potential for significant upside. Ackman said Wednesday that he finished unwinding the hedges on Monday, reaping $2.6 billion in proceeds

with more than 522,000 people infected globally. The number of people confirmed to have died as a result of the virus has now surpassed 23,500.

The virus’s proliferation has been declared a pandemic by the World Health Organization, meaning it is spreading rapidly in different parts of the world. More than 180 countries have confirmed cases so far.

The epicentre of the coronavirus is now Europe, with the largest number of confirmed cases in Italy, and death tolls growing more quickly in Italy and Spain than they did in China at the same stage of the outbreak.

(80) US companies raise $25bn as bond market thaws | Financial Times

Spreads at 3 to +4X over respective 10 & 30 yr. Treasuries over last year

US companies raise $25bn as bond market thaws

ExxonMobil, PepsiCo and Verizon lead list of issuers paying higher interest rates to raise cash

16 hours ago

ExxonMobil, PepsiCo and Verizon were among nine US companies that raced to borrow money on Tuesday as improved market conditions opened the door for the groups to sell tens of billions of dollars in investment-grade corporate bonds.

Companies across the globe have worked to fortify their balance sheets over the past two weeks by securing new loans from banks. On Tuesday, the corporate bond market thawed, providing an opening for better quality groups to issue debt — albeit at higher rates than in recent months.

...

"Companies should use any window they can to access liquidity at the moment," said John McClain, a portfolio manager at Diamond Hill Capital Management. "I believe these deals should function smoothly but they will be the first test of the new economic reality we are in."

The nine companies borrowed $25bn, according to FT calculations, with recently downgraded oil and gas producer Exxon clinching $8.5bn, the largest borrower of the day...

However, institutional investors on Tuesday demanded significantly higher payouts, reflecting fears of an economic slowdown. Exxon raised $2bn of the $8.5bn through new 10-year debt, which was priced to yield 240 basis points over a similarly maturing US Treasury, or 3.48 per cent. Less than a year ago it issued 10-year bonds with a so-called spread of just 75 basis points, which yielded 2.44 per cent at the time.

Wireless carrier Verizon, beverage group PepsiCo and Bank of America faced similar investor demands. The maker of Pepsi and Lays potato chips secured $6.5bn on Tuesday in the second-largest bond offering, with 30-year debt sold to investors at a spread of 200 basis points and a yield of 3.65 per cent. That compared with the premium of 80 basis points it paid last July when it issued a 30-year bond.

Hold on, the shock to the oil market is going to spread.

Photographer: Andrew Burton/Getty Images

To get John Authers' newsletter delivered directly to your inbox, sign up here.

OPEC+: A 24-Hour View

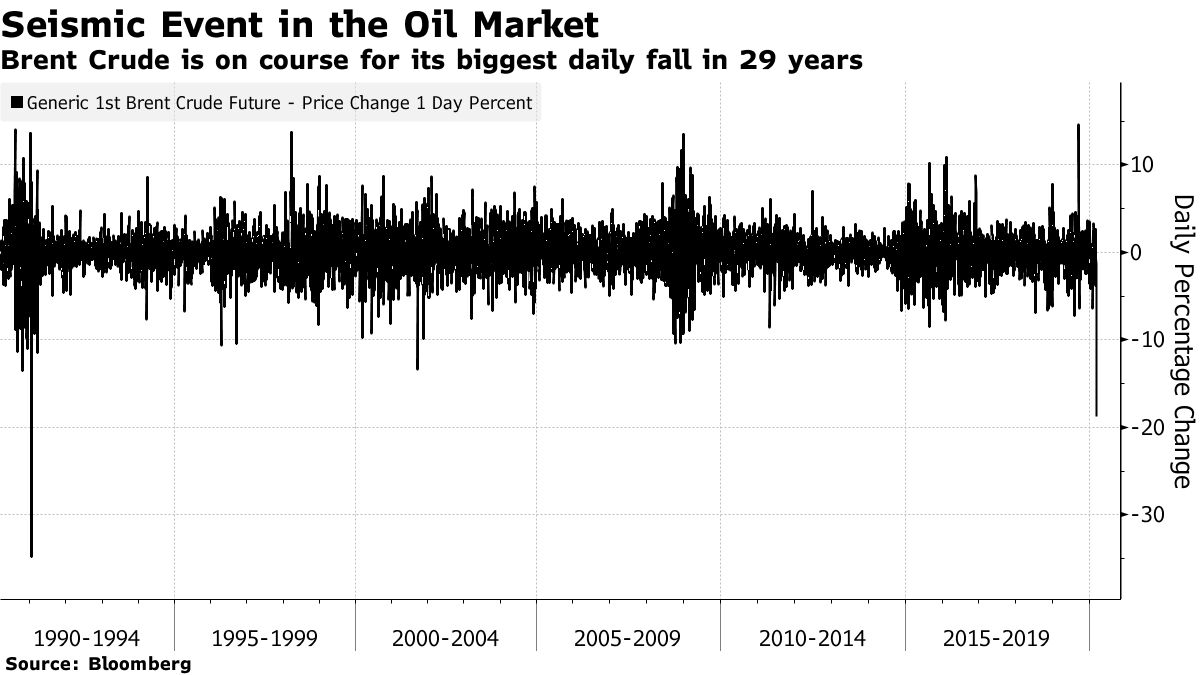

Coronavirus. That will be the first and last time this column mentions that word. Despite the weekend's many developments in the epidemic, there is a new issue to drive the markets. Like the dreaded disease, its effect is to take an already disquieting market trend and make it far more extreme. The breakdown of the OPEC talks in Vienna on Friday, followed by Saudi Arabia's announcement that it would abandon attempts to limit supply, and instead aim to increase market share, has driven a historic fall in the oil price.

With Brent and West Texas Intermediate crude both down more than 20% when trading began in Asia, this was on course to be the worst day for the oil price since January 1991, when a coalition was fighting Iraq over its invasion of Kuwait:

Moves this dramatic can create quite a shock. This could be good news for beleaguered airlines, whose fuel will be much cheaper, and it should provide a broad economic stimulus as motorists and industrialists see fuel costs reduced. But those benefits take time to make themselves felt.

In the meantime, this will put immense pressure on anything that benefits from a high oil price. An immediate effect will be on the U.S., which has profited from the shale oil boom. The economics of that industry now come under threat — which is precisely the purpose of allowing prices to drop so far. Shale operators tend to be heavily leveraged and so now face a great risk of bankruptcy, which will hurt banks, and credit investors. That puts pressure on the Federal Reserve to cut rates further. The market now predicts the Fed will have to cut another 75 basis points off the overnight fed funds rate at its meeting this month.

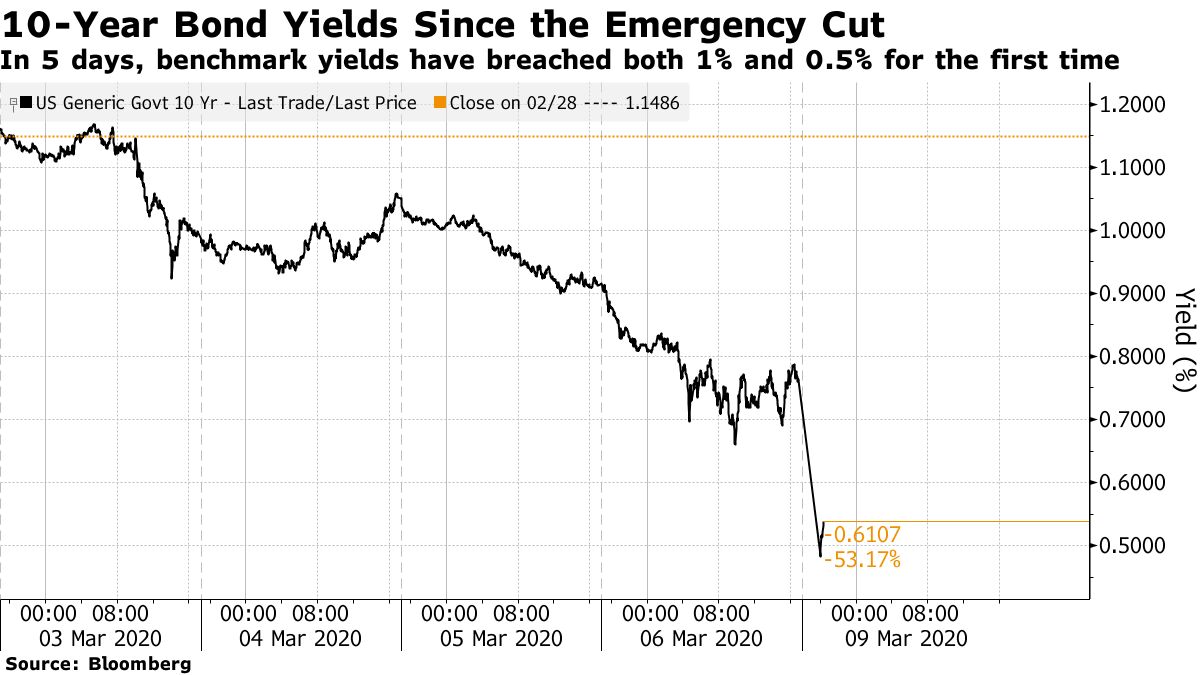

Thus the virtual collapse of OPEC has led to a further collapse in U.S. interest rates. This is what has happened to the 10-year Treasury yield since the emergency cut of 50 basis points announced last Tuesday:

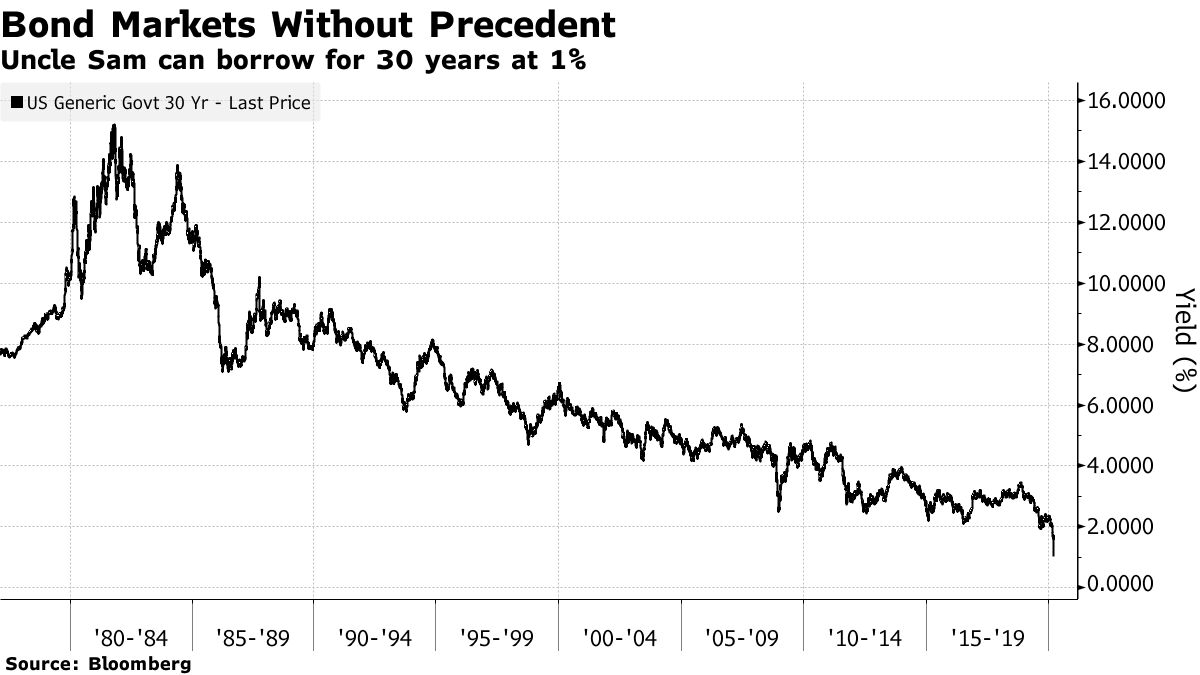

If the epidemic and the Fed's response to it brought 10-year yields below 1% for the first time, dissension among oil producers has brought them below 0.5% less than a week later. Possibly even more remarkable is the fall in the 30-year yield, which dropped below 1% at the Asian opening, easily its lowest ever:

Central banks want to show they can raise inflation. This sudden fall in fuel costs makes that far harder, at a point when the response to the emergency cut showed that the market was already losing confidence in their ability to do so. The result has been a sharp convergence of U.S. and euro zone yields, to the narrowest in six years:

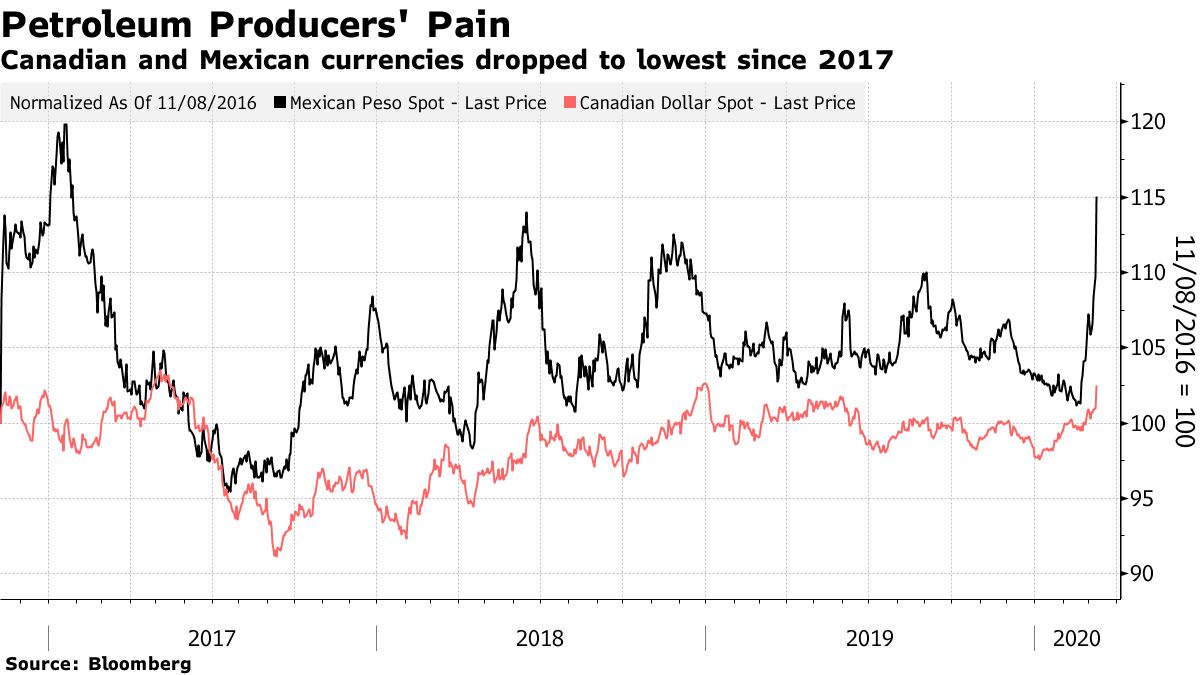

Normally when people are scared, they seek sanctuary in dollars. This is particularly true when oil falls; the dollar tends to be inversely correlated with oil, and shot up during the last major leg down for crude in late 2014. That isn't happening this time, at least so far. The dollar has fallen to its lowest versus the Japanese yen since 2016, while gold has topped $1,700 per ounce for the first time in 12 years.

The dollar can at least enjoy some strength against petro-currencies, which benefit from higher oil prices. It strengthened sharply against the Mexican peso and Canadian dollar in Asian trading.

In the long term, there is an opportunity for everyone to benefit from cheaper fuel prices. Historically low bond yields are also effectively an invitation from the market for governments to borrow as much as they like, so if ever there was a time for fiscal expansion, this is it.

In the short term, we should expect a run on bank stocks, and energy stocks. Faced with such evidence of deflation, cyclical stocks will come under pressure. So will everything in what might be called the emerging market complex — industrial metals, as well as emerging market stocks, debt (which if denominated in dollars will be much harder to pay off), and currencies.

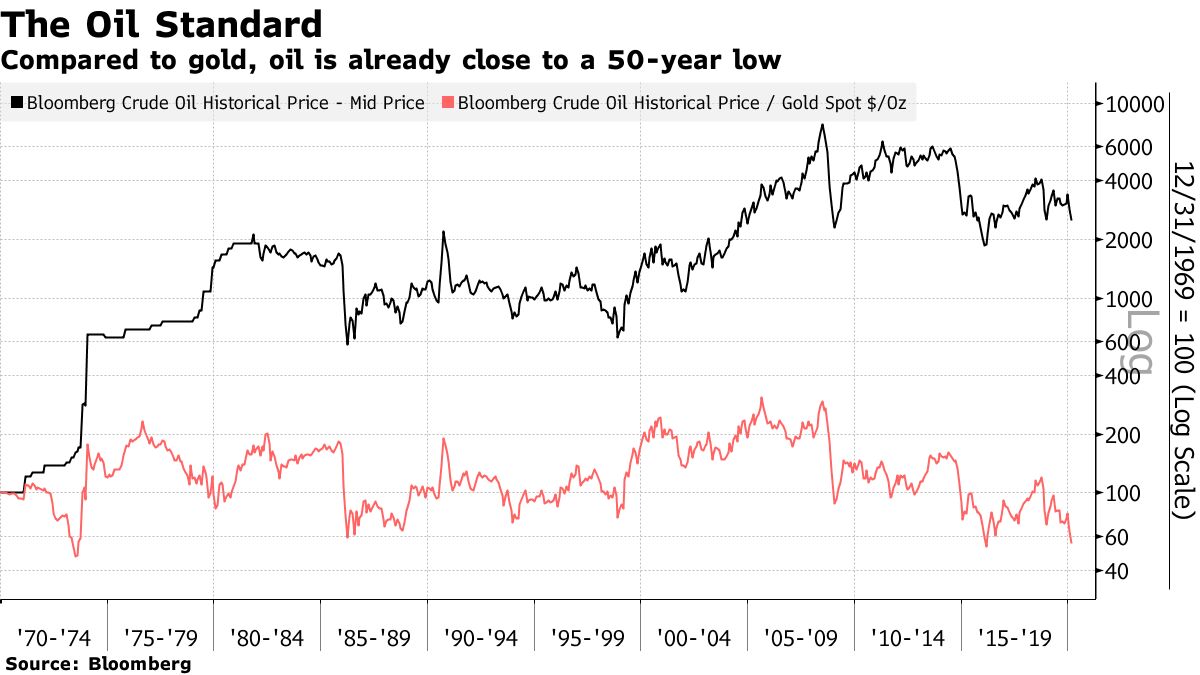

The Oil Standard: A 50-Year View

Having said all that, looking too closely at the drama following the OPEC breakdown might miss the point. This looks like a truly historic juncture, of the kind that comes along only every few decades, as the international financial order shifts.

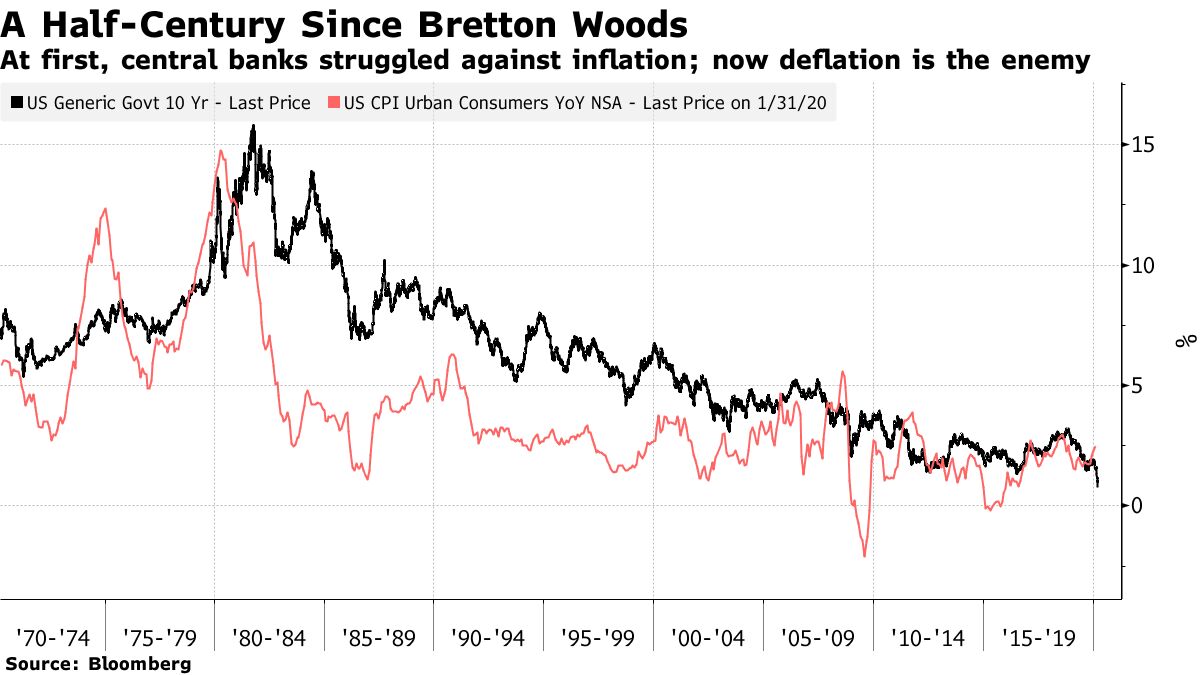

After the war, the developed world was governed by the Bretton Woods accords, which tied all currencies to the dollar, which was in turn pegged to gold. It was a looser form of a gold standard, and survived until 1971. That was when Richard Nixon ended the gold peg, realizing that it had become too great a burden for the U.S., and stood in the way of the expansionary fiscal policy he was hoping to adopt ahead of his re-election campaign.

The result was a huge shock to the world order. With the gold peg gone, the financial system adopted a new anchor, which was oil. In a book published 10 years ago, I tried describing the system that replaced Bretton Woods as an Oil Standard. Effectively, producers tried to defend themselves against the declining buying power of the dollar by hiking prices, so as to keep the price of oil in gold terms effectively constant. The oil/gold ratio measures how much gold you would need to pay to buy a certain amount of oil. As the chart shows, it ended the 1970s almost exactly where it had started, despite the massive increase in dollar terms.

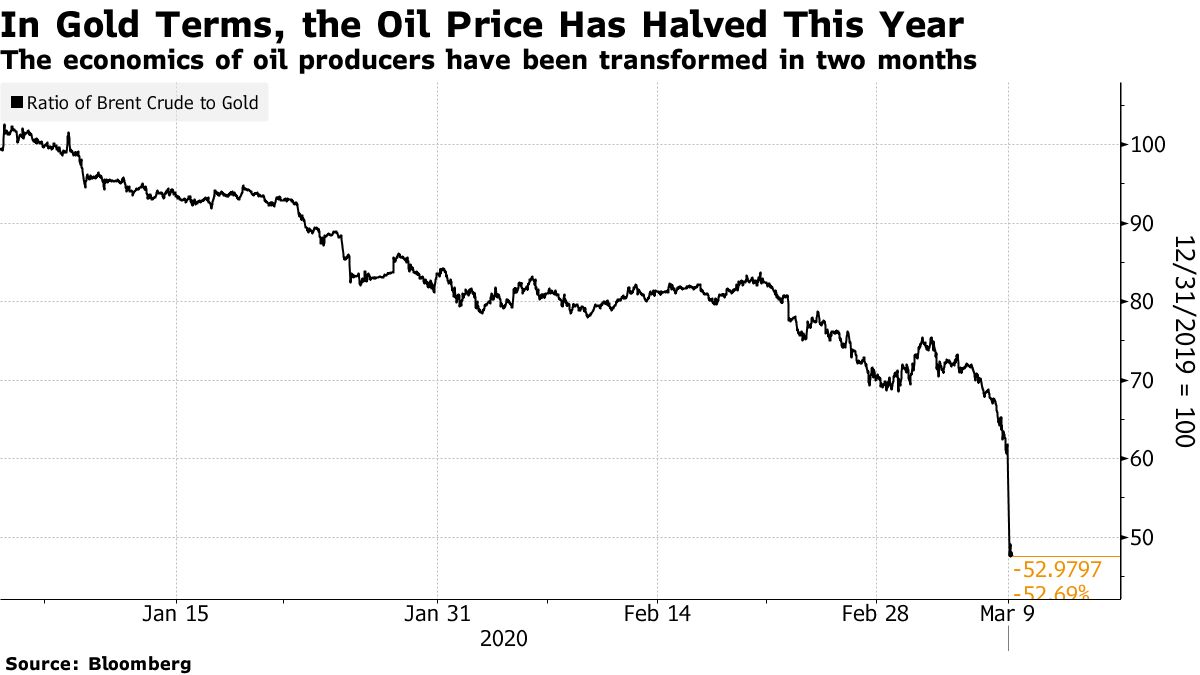

The chart uses Bloomberg's historic oil prices, which appear monthly, and pre-dates the latest market drama. Once updated, it will show the oil/gold ratio reached an all-time low, having already halved this year:

The Oil Standard era ended in the early 1980s. Markets — and everyone else — had lost faith in the ability of central banks to control inflation. Paul Volcker arrived at the Fed, raised rates more than anyone thought he would dare, provoked a recession, and convinced everyone that central banks could control inflation after all. In conjunction with the Reagan/Thatcher approach to economic management, and then the collapse of the Soviet Union and the resurgence of China, that ushered in a quarter-century of triumphalism for a new model anchored by broadly trusted central banks.

That foundered in the financial crisis of 2007-09. Now we have reached a new juncture, where the fear is that central banks cannot control deflation. For the post-crisis decade, the U.S. has managed to stay distinct, thanks in part to the privilege of the world's reserve currency, and in part to the superior success of its corporate sector. It has done this even as Japan and Western Europe have sunk into negative interest rates, while the emerging markets have stagnated. The twin shocks of the epidemic and the oil price now appear to have wounded confidence that the U.S. can stand alone.

It certainly looks as though the world has at last arrived at a point that it appeared to have reached a decade ago. Some new financial order, to replace Bretton Woods and the system that Volcker built to replace it, is now needed. A decade of monetary expansion has delayed the issue. It is hard to see how it can be delayed much further. It would be wise to brace for disruption to match what was experienced at the end of the 1970s and the beginning of the 1980s.

One of the world's largest manufacturers of the ASIC devices that are used to "mine" cryptocurrency looks like a total Scam.

"investigation of this bitcoin mining machine maker revealsundisclosed related party transactions, irregularities involving many customers and distributors, as well as a business model that we view as broken. Regardless of your outlook on the future of Bitcoin,we believe that CAN's business is simply far worse than promoted. "

"In the three months or so since listing, [$CAN] has seen its share price collapse by almost half, from $9 to around $4.70 at pixel time (despite a rather unusual 80 per cent one-day surge in the middle of last month). And that's in a period during which bitcoin has climbed about 15 per cent."

Norwegian Air shares plunge to 15-year low as coronavirus adds to pressure. They raised NKr5.6bn -- $605MM-- in equity in 3 capital raisings in past 2 years + NKr1.5bn in convertible bond and extended debt maturities on NKr3.4bn of debt...But its market capitalisation on Monday was just NKr2bn.

Needs to raise +/- NKr3bn to meet a challenging market and not find itself in the same situation next year when it faces repayment of a €250m bond.

An excellent piece on Venezuela by Anne Applebaum in The Atlantic, showing that what we are witnessing there is but a microcosm of so many of the ailments we see in so many countries' political systems / situations throughout the world today.

Long read, but worth it.

Venezuela Is the Eerie Endgame of Modern Politics

Citizens of a once-prosperous nation live amid the havoc created by socialism, illiberal nationalism, and political polarization.

Last month, Juan Guaidó appeared in Washington in the role of political totem. Venezuela's main opposition leader—the man who is recognized by that country's National Assembly, millions of his fellow citizens, and several dozen foreign countries as the rightful president of Venezuela—was one of the special guests at the State of the Union address. President Donald Trump welcomed Guaidó as living evidence that his own administration was "standing up for freedom in our hemisphere" and had "reversed the failed policies of the previous administration"; he called Venezuela's current leader, Nicolás Maduro, an illegitimate ruler whose "grip on tyranny will be smashed and broken." He gave no details of how that would happen. Trump, who has never been to Venezuela or shown any prior interest in it—or, for that matter, shown any interest in freedom anywhere else —presumably knows that the country matters to some voters in South Florida. To their credit, members of Congress gave a bipartisan standing ovation to Guaidó nevertheless.

Trump is not the only world leader to cite Venezuela for self-serving ends.

Regardless of what actually happens there, Venezuela—especially when it was run by Maduro's predecessor, the late Hugo Chávez—has long been a symbolic cause for the Marxist left as well. More than a decade ago, Hans Modrow, one of the last East German Communist Party leaders and now an elder statesman of the far-left Die Linke party, told me that Chávez's "Bolivarian socialism" represented his greatest hope: that Marxist ideas—which had driven East Germany into bankruptcy—might succeed, finally, in Latin America.

Jeremy Corbyn, the far-left leader of the British Labour Party, was photographed with Chávez and has described his regime in Venezuela as an "inspiration to all of us fighting back against austerity and neoliberal economics."

Chávez's rhetoric also helped inspire the Spanish Marxist Pablo Iglesias to create Podemos, Spain's far-left party. Iglesias has long been suspected of taking Venezuelan money, though he denies it.