We know that there is a law called the debt ceiling. We also know that we will (again) hit that limit early in 2011. Many think that this will be a line in the sand fight with the new Congress. Phooey. According to the CBO report, suspending issuance of maturing cash management bills in the supplementary financing program will cost $200 billion; suspending flows and redeeming securities in government accounts, $124 billion; from the civil service retirement fund, "at least" $200 billion; from the exchange stabilization fund, $20 billion; and swapping debt with the federal financing bank, $15 billion. Total: $560 billion.

Conclusion: If there is to be a fight over the debt limit, it could be a long one.

The CBO is speaking with forked tongue in this report. A critical issue: How do we define what debt is at the federal level?

There are so many components to the puzzle. I give the CBO an A+ for this position:CBO believes it is appropriate and useful to policymakers to include Fannie Mae’s and Freddie Mac’s financial transactions with other federal activities in the budget. The two entities do not represent a net asset to the government but a net liability — that is, their impact on the government’s financial position is a negative one.

So how does CBO actually account for F/F? It gets a D- for this:

Neither CBO nor the Administration currently incorporates debt or MBSs issued by Fannie Mae (FNMA.OB) and Freddie Mac (FMCC.OB).That’s interesting. They say they “should” do it, but they don’t. Who makes that decision?

The Administration’s Office of Management and Budget (OMB) makes the ultimate decision about whether the activities of Fannie Mae and Freddie Mac will be included in the federal budget.

The White House decides which categories of debt are included when determining what constitutes debt? That is convenient. When did that happen? We are not talking chicken scratch here. The good folks over at the Fannie and Freddie have piled up $6 trillion in debt. We would blow out the debt ceiling set by Congress by over 40% if that came on the books. So it stays off the books. But the debt is staring us in the face. Funny system.

This also caught my eye:

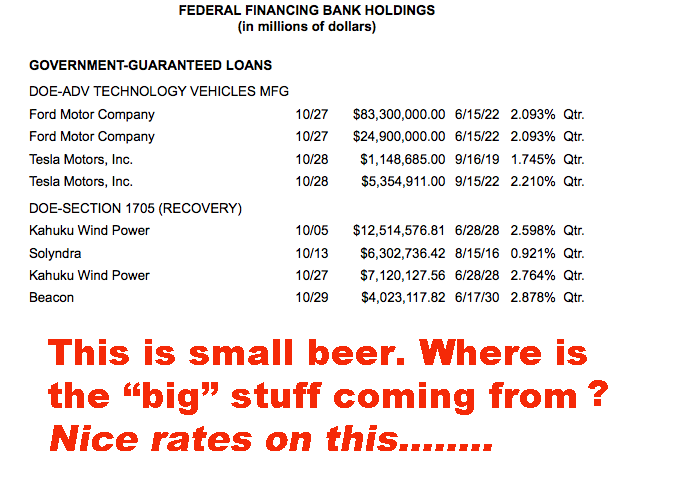

Payments of interest from the FFB to the Treasury have been less than $1 billion annually in recent years but are projected to increase (to as much as $6 billion) because of higher loan activity (particularly by the Department of Energy's Advanced Technology Vehicles Manufacturing program and the Rural Utilities Service). As of September 30, 2010, the FFB portfolio totaled $60 billion.

Hello, what is this? For interest to rise at the FFB from $1 billion to $6 billion, it would have to imply that there is at least a four- or five-fold increase in the balance sheet. This means that there is a plan to grow the FFB by $250 billion. Who is going to be the beneficiary of that? That is a hell of a lot of money. Is the FFB going to fund a solar build-out? The existing portfolio of Department of Energy loans:

Another (minor) data point of interest: The federal government has a number of trust funds that are used as accounting vehicles to store up IOUs from the government. The principal accounts and current holdings:

Social Security Trust Fund…….2.6t

Civil Service Retirement Fund...0.8t

Military Retirement Fund……...0.3t

Medicare……………………….0.3t

All others…….………………...0.6t

Total:…………………………..4.6 trillion

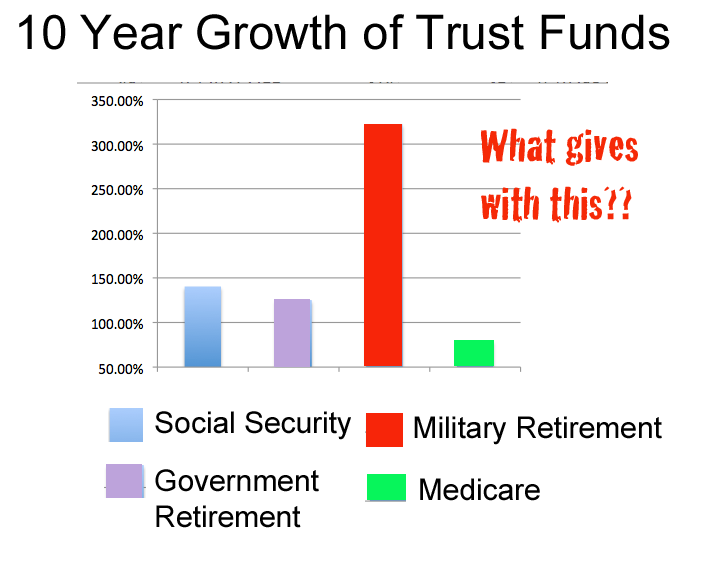

These funds are all anticipated to grow over the next decade. One has a growth rate that is way out of whack with the others:

The Military Retirement Fund is growing at three times the rate of the others. The raw numbers are $282 billion for 2010 and $1.012 trillion for 2020. That's a 10-year increase of $730 billion (a 350% increase). What is that about? Are we planning on a new war, or have we just not accounted for the retirement costs of the military properly over the past decade or two? I suspect (hope) it is the latter.

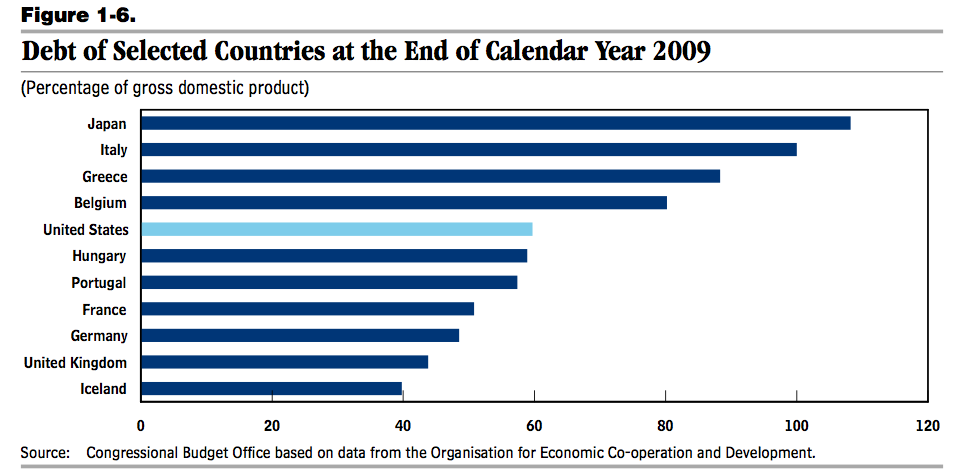

We have all seen a form of this chart elsewhere. It is nothing to be proud of. Yes, there are a few countries in worse shape than us. But Italy, Greece and Belgium are now making front-page news with their debt. And the U.S. will have a different outcome than Japan.

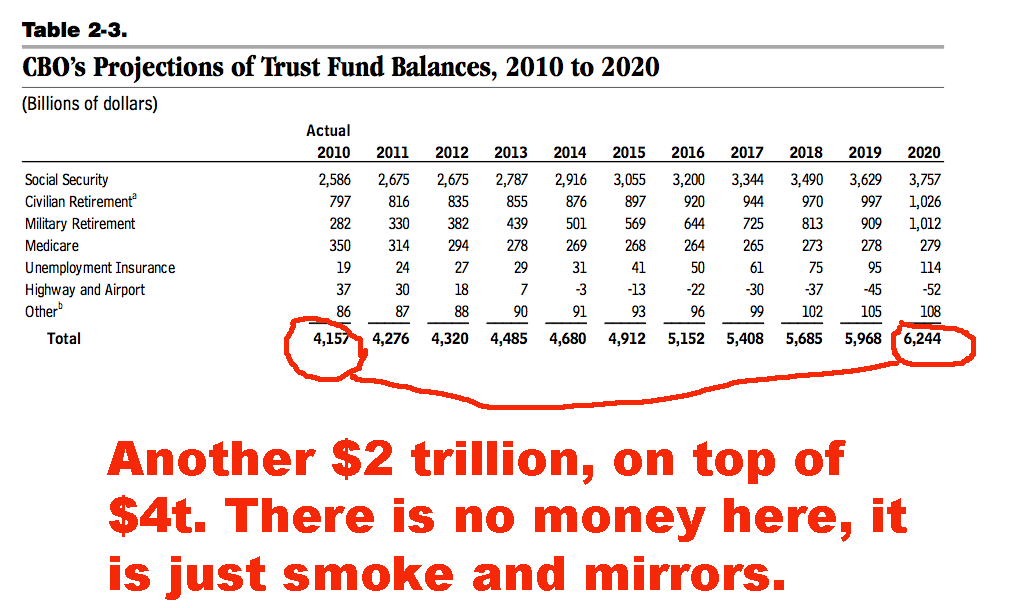

This chart of trust fund assets is central to our problem. Notice that these funds are scheduled to grow by more than $2 trillion. It sounds nice that the nation has trust funds where money is squirreled away someplace safe -- money that can be used to pay bills (Social Security) when they come due over the next 20 years.

But there is no money in the trust funds. They have IOUs that obligate future taxpayers to come up with the cash when needed. The trust funds have nothing to do with “savings” in the traditional sense.

This has been going on since 1983, when Greenspan created the accounting gimmick and the huge surpluses that followed. The fact is we do have future liabilities, and there have been some savings set aside for that. But the money has been spent on funding past deficits. So, really, there are no savings.

I am not sure there is a fix to this problem. I do know that the bills on this are coming due in the next five years or so. I don’t think we will make it another 10 years without having to confront this problem.

Debt Factoids on Our National Debt Are Puzzling - And Scary - Seeking Alpha

No comments:

Post a Comment

___________________________________

Commented on The MasterFeeds